There's a window open in London's property market right now. It won't be there forever.

Prices have softened. Developers need early buyers. The capital's fundamentals — global demand, chronic undersupply, world-class connectivity — are exactly as robust as they've always been. And two extraordinary new developments, Westminster Tower on the Albert Embankment and Wimbledon Bridge House in SW19, are sitting at precisely the right intersection of quality, location and timing.

This is a piece about cold, clear numbers — what London's property market looks like right now, where independent forecasters say it's heading, and why buying off-plan today with Imperia Broker could be one of the most rewarding financial decisions of the next decade.

Whether you're an international investor looking to place capital in one of the world's most transparent and liquid markets, or someone who simply wants to secure a stunning home in London before prices recover — read on.

Table of Contents

The State of Play: London Property in 2026

Let's start with the full picture.

London has not been the easiest market over the past few years. After explosive growth post-2008, prices stagnated through much of 2015–2025, growing just 16% against 44% across the rest of the UK. In the year to February 2026, London prices fell 3.3% according to the ONS House Price Index — making it technically the weakest-performing region in England by headline figures.

But here's what that headline misses entirely.

When the broader market is soft, developers must compete for early-stage buyers. That means better pricing, more flexible payment structures and stronger incentives. You lock in today's softened value. You complete in 2027 or 2028. You collect on the upswing. We've covered the broader thesis of where London capital is flowing in 2026 in more detail — Bayswater, Farringdon and Old Oak Common are the macro context that makes specific off-plan plays like Westminster Tower and Wimbledon all the more compelling.

And the upswing is coming.

The Forecasts: Cumulative Growth of 13–18% by 2030

The major estate agencies are in rare agreement: London is at or very near its cyclical floor, and the trajectory from 2027 onwards is meaningfully upward.

Savills projects year-on-year growth of 4%, 5%, 5.5% and 4% for the years 2027 through 2030 respectively — driven in part by forecasted wage growth of 22% between 2025 and 2029. Knight Frank goes slightly higher, forecasting 3% in 2027 and 4% in 2028.

For context: if you buy a Westminster Tower three-bedroom apartment at £4,800,000 today and Savills' 13.6% forecast plays out, the same apartment is worth approximately £5,452,800 at completion — a paper gain of over £650,000 on an asset you haven't yet moved into.

At Wimbledon Bridge House, a two-bedroom apartment at £1,235,000 appreciating 13.6% means a completion value in the region of £1,403,000 — a gain of nearly £168,000.

These are projections, not guarantees. But they are the considered forecasts of the largest residential research operations in the UK, and they are structurally supported by one fact that hasn't changed: London does not build enough homes.

The Greater London Authority target is 52,000 new homes per year. Actual completions run closer to 35,000. High material costs, labour pressures and planning complexity mean that gap is not closing. Supply is constrained. Demand is not going anywhere.

The Off-Plan Advantage: Locking In Below Tomorrow's Value

Off-plan property is one of the few legal ways to buy an asset at a structural discount to its future value. The mechanics are straightforward, and the numbers are well-documented.

Early-stage off-plan launches typically price 10–15% below projected completion value. This is the commercial logic of pre-selling units to fund construction. You are providing capital at risk in exchange for price advantage. And in London, where the market has been flat, that advantage can be even more pronounced because developers need to move units.

What this means in practice: you buy a unit off-plan today at £500,000. The same unit, at completion in 2027–28, is expected to be worth £550,000–£575,000 based on comparable completed stock — before any general market appreciation. Add Savills' projected 4–5% annual growth in 2027–28 and you have a property worth substantially more than you paid, from day one of ownership.

There is a second structural advantage: payment staging. Unlike buying a completed property — where your capital is locked in immediately — off-plan purchases allow you to reserve a property with a deposit and stage your payments over the construction period.

At Westminster Tower, the structure is:

- £10,000 reservation fee

- 20% of purchase price on exchange (21 days later)

- 5% of purchase price six months after exchange

- 75% on completion

At Wimbledon Bridge House:

- £2,500 reservation fee

- 10% on exchange (28 days later)

- 10% twelve months after exchange

- 80% on completion

Your capital is working more efficiently. You are not servicing a mortgage or tying up your full purchase price for two years while the building completes. And if values rise during construction — as they historically do in recovering markets — your equity builds before you've fully committed.

Westminster Tower: The Most Prestigious Address in Zone 1

Address: 3 Albert Embankment, London SE1 7SP

Completion: Q3/Q4 2027

Developer: London Square (Aldar Group)

There are very few addresses left in London where you can stand in your living room and look directly at the Houses of Parliament, Big Ben and Westminster Bridge. Westminster Tower is one of them.

Sitting on the south bank of the Thames, this 17-storey refurbishment of a 1983 tower offers 30 residences — two-bedroom, three-bedroom and a singular four-bedroom duplex penthouse — all with protected, uninterrupted views across one of the world's most recognisable skylines.

The interiors are designed by Mustard & Linen, whose brief was to create "a tranquil and luxurious haven" inspired by the tower's riverside position. Think engineered timber chevron flooring, full-height veneer kitchens with fluted glass cabinetry, Miele appliances throughout (including an integrated drinks cooler and boiling water tap), engineered stone countertops and bathrooms with freestanding baths, brushed copper brassware and ceiling-mounted shower heads.

The building also features a home automation system for lighting and audio, comfort cooling in all rooms and a Portland stone exterior with triple-glazed bronze-detailed windows.

Residents have exclusive access to a 24-hour concierge, a Reading Room with private meeting booths, a Fitness Suite, a Screening Room and a Residents' Lounge.

The location is unrivalled for connectivity. You're a 3-minute walk from Vauxhall Station (Victoria line, National Rail), 5 minutes from Lambeth Palace, 8 minutes from St James's Park on foot, and 47 minutes by road from Heathrow. Victoria is a 4-minute Tube ride. Bond Street is 13 minutes.

Westminster Tower: Current Pricing (March 2026)

Service charge: £13.50 psf per annum

Lease: 999 years from January 2027

Note that several units are already sold — including Apartment 201 (The Lexham, 2nd floor), The Vincent (4th floor, 3 bed) and the Parliament apartment on the 11th floor. At this stage of launch, the best units go first. For the full set of available units at Westminster Tower and other London investment properties in our current catalogue, contact our team.

Rental Income Potential at Westminster Tower

The developer's own estimated rental figures are conservative by London prime market standards:

- 2-bed apartments: £6,500–£7,583 PCM

- 3-bed apartments: £10,400–£13,000 PCM

To put this in context: a 3-bed Parliament apartment at £4,850,000 generating £10,400 PCM produces a gross yield of approximately 2.6%. At £13,000 PCM, that's 3.2%.

These are at the lower end of prime London yields — but they are not why you buy Westminster Tower.

Prime Central London delivered average capital growth of 63.5% between 2007 and 2017 (Savills). Between 2007 and 2024 the area saw values roughly double despite two major crises.

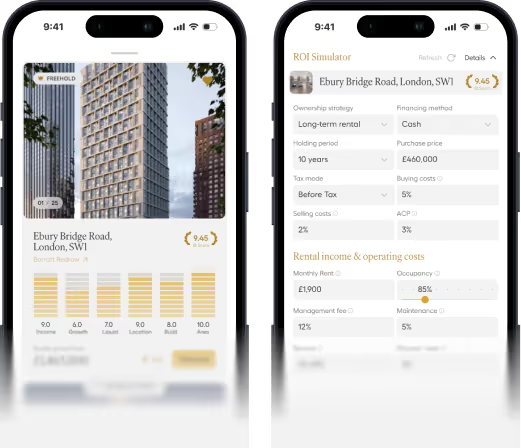

The yield here is a holding return. The capital appreciation is the investment case. That distinction — and where Westminster Tower sits on it — is exactly what our IB Score methodology captures across six factors: Income, Growth, Liquidity, Location, Build and Safety.

Wimbledon Bridge House: The Premium Suburb Play

Address: 1 Hartfield Road, London SW19 3RU

Completion: Q3 2028

Developer: London Square

If Westminster Tower is the ultra-prime capital appreciation story, Wimbledon Bridge House is the yield-and-growth combination that makes more sense for investors and owner-occupiers alike.

Wimbledon is not a suburb on the way up. It is already at the top. Knight Frank named it the #1 premium high street in the UK in November 2025. It is home to some of London's highest-ranked independent schools, 900 acres of green space, and the global draw of the All England Lawn Tennis Club — just one mile from the development. The station is a two-minute walk.

The development itself is a seven-floor building of 123 residences — studio, one-bedroom, two-bedroom and two exclusive three-bedroom penthouses on the seventh floor — designed by Johnson Naylor (Clerkenwell's most respected interior architecture practice). The ground through second floors feature a restaurant, retail, co-working spaces, a members' gym and private lounge.

Two palette options — Bosca (rich forest tones, dark woods, deep green bathroom vanities) and Folia (soft creams, sage, light timber) — let buyers personalise their home's character.

There are Juliette balconies and terraces on selected units from the fifth floor upward. There is a 999-year lease. And on the data point that matters most to investors right now, Wimbledon posted +3.4% year-on-year price growth in Q2 2025 — outperforming prime central London by a significant margin, with a £12 million record sale in the area the same period.

Wimbledon Bridge House: Current Pricing (March 2026)

One-Bedroom Suites (45 sq m / 486 sq ft)

One-Bedroom Apartments (49–55 sq m)

Two-Bedroom Apartments (71–114 sq m)

Service charge: £6.00–£6.25 psf per annum. Parking: £40,000 (selected 2 and 3-bed only). Lease: 999 years.

Rental Income Potential at Wimbledon Bridge House

A 1-bed apartment at £587,500 generating £2,500 PCM = gross yield of ~5.1%. That's genuinely competitive for prime London, and well above what you'd expect at this address once completed and comparable to finished stock.

The Yield vs. Capital Growth Matrix: Where Do These Properties Sit?

Every investor needs to decide what they're optimising for. Here's an honest map:

For investors seeking maximised rental yields in excess of 6–7%, northern cities like Manchester and Liverpool offer higher returns on lower capital. That is a real and valid alternative. But those markets cannot offer what London offers: unmatched liquidity, legal security, global demand, currency-of-last-resort status and a 999-year lease in one of the world's most recognisable cities.

London's average property value in January 2014 was £355,000. By 2024 it was £523,000 — a 47% increase despite a decade of relative stagnation. After 2008's financial crisis, London prices grew 63.5% in the following ten years. The city has a habit of rewarding those who buy at the bottom of the cycle and hold.

We believe 2026 is that moment again.

The IB Score Verdict: Both Developments Scored

A strategy map shows fit; the IB Score shows the asset. Both developments have been rated 1–10 across the six factors, on the same scale as any other property we assess.

Westminster Tower — IB Score 7.0 / 10 (Strong)

Westminster Tower is a capital-preservation asset: location, build and safety carry it, while income and liquidity reflect the economics of prime new-build rather than any weakness.

Wimbledon Bridge House — IB Score 8.0 / 10 (Strong)

Wimbledon scores strongly across every factor, led by liquidity — the balance that makes it the better fit for investors weighing yield and growth together.

A Note for International Investors: Why London, Why Now, Why Imperia Broker

London is the most international property market in the world. The legal system is transparent, property rights are iron-clad, there are no restrictions on foreign ownership, and the UK's common law framework is trusted by buyers from every jurisdiction. That is not true of every market that promises high returns.

At Imperia Broker, we work with international clients from the UAE, Asia, the Americas and across Europe. We understand that buying in another country involves questions that go far beyond the property itself.

Here is what we handle for you:

Legal and compliance. Both Westminster Tower and Wimbledon Bridge House are offered with a vetted panel of solicitors — including international firms with offices in Singapore, Dubai and Hong Kong — who specialise in UK property transactions for overseas buyers. We connect you with the right legal representation from the moment you reserve.

Currency and financing. Our in-house experts understand non-UK income structures, multi-currency wealth and international mortgage solutions. Whether you are buying in USD, AED, HKD or SGD, we manage the FX timing and financing structure in-house, ensuring your capital works as efficiently as possible from the moment you reserve.

Tax structuring. Stamp Duty Land Tax (SDLT) applies to property purchases in England. Overseas buyers pay an additional 2% surcharge on top of standard rates. This is a known, quantifiable cost that we factor into your investment modelling from the outset — no surprises. We work with specialist property tax advisors who can advise on optimal purchasing structures (personal vs corporate, SPV, trust) based on your residency and portfolio goals.

Property management. Once your property completes, you have options — and we handle all of them. Through Staymo — the London short-let operator that backs Imperia Broker — we can manage your property across all letting strategies: short-term lets (ideal for the tourist and corporate short-stay market, particularly relevant for a riverside address like Westminster Tower), mid-term lets of one to six months targeting relocating professionals and corporate tenants, and traditional long-term tenancies for stable, low-maintenance income. Staymo handles everything — listing, guest or tenant management, check-ins, maintenance coordination and monthly reporting. You receive the income. You don't receive calls about broken boilers.

Resale. London's new-build market is highly liquid. Both London Square developments carry strong brand recognition among the buyer community. When the time comes to sell — whether at completion, three years later or at the ten-year mark — we will be with you for that transaction too.

Buying property in a foreign country should feel like an opportunity, not an obstacle course. That is precisely what we are here for.

Comparing London to Global Competitors

International investors are rarely choosing between London and Manchester. They are choosing between London and Dubai, London and Singapore, London and New York. Here is the honest picture:

Dubai offers higher headline yields, and it has attracted significant investor interest over the past decade. But it is worth being clear-eyed about the risks. The region faces ongoing geopolitical instability, and its economy is heavily dependent on oil, tourism and global capital flows, all of which are sensitive to regional disruption. Property rights, while improving, remain less robust than in the UK's common law framework, and the regulatory environment continues to evolve in ways that are not always predictable for foreign holders. For investors placing long-term capital, the question is not just what Dubai yields today — it is whether the foundations beneath that yield are stable over the next decade. London's foundations have been tested repeatedly and held.

Singapore offers security but imposes punishing Additional Buyer's Stamp Duties on foreign purchasers (up to 60%). New York is opaque, expensive to transact in and heavily regulated. London's combination of transparency, liquidity, global demand and legal certainty remains unmatched. For wealth preservation with meaningful upside, it occupies a category of one.

Our Developer Partners: Aldar and London Square

Not all developers are equal. And not all broker relationships with developers are equal either.

Both Westminster Tower and Wimbledon Bridge House are built by London Square, one of the UK's most decorated residential developers, founded in 2010 and now part of the Aldar Group — one of the Middle East's largest listed real-estate groups, headquartered in Abu Dhabi.

This parentage matters enormously for buyers. Aldar's backing means London Square operates with a level of financial solidity that smaller independent developers cannot match. Construction delays, developer insolvency and incomplete projects are the principal risks of off-plan investment. With Aldar behind London Square, those risks are materially reduced.

The group has delivered over 30 award-winning developments in London and received more than 60 industry accolades for design and customer service.

Every home comes with a 10-year structural build warranty and a 2-year London Square Customer Care period.

Imperia Broker is a direct partner of both London Square and Aldar. This is not an arm's-length relationship through a sales portal. We work directly with the developer's sales teams, giving our clients privileged access that the open market simply does not offer:

- Pre-launch and early-release pricing before units are made publicly available

- Priority unit selection — the best floors, the best aspects, the corner units and the river views go to direct partners first

- Exclusive stock that never reaches the property portals or general agent networks

- Direct communication with the developer on buyer queries, legal progress and build updates

- Developer incentives and upgrades available only through channel partners

When you enquire about Westminster Tower or Wimbledon Bridge House through Imperia Broker, you are not competing with hundreds of other buyers on a public listing. You are accessing the development through the preferred route — the one the developer's own team uses to place their best clients.

The Numbers, Assembled: A Worked Example

Let's model a specific scenario for a Wimbledon Bridge House 1-bed apartment at £587,500 (Plot 1, First Floor, North-facing), completing Q3 2028.

Purchase costs (buyer, overseas national)

- Purchase price: £587,500

- SDLT (standard + 2% overseas surcharge): ~£37,500

- Legal fees + survey: ~£5,000

- Total acquisition cost: ~£630,000

Payment staging

- Reservation (now): £2,500

- Exchange (28 days): £58,750 (10%)

- Month 12 post-exchange: £58,750 (10%)

- Completion (Q3 2028): £470,000 (80%)

At completion (Q3 2028) — conservative scenario using Savills projections

- Market value (13.6% cumulative growth applied to £587,500): ~£667,400

- Equity on day one of ownership: ~£37,400 before any rental income

Rental income (based on developer estimates)

- £2,500 PCM / £30,000 per annum gross

- Less management fees (12%): £26,400

- Less service charge (£6.25 psf on 560 sq ft): ~£3,500/yr

- Net income: approximately £22,900 per annum

- Net yield on purchase price: ~3.9%

Over a 5-year hold from 2028 to 2033 (during which London prices are forecast to continue recovering)

- Net rental income: ~£114,500

- Further capital appreciation (conservative 2% per year post-2028): ~£67,000

- Total return over 7 years from today: ~£218,400 on £630,000 invested = 34.7% total return

This is not an aggressive scenario. It uses conservative forecasts and full cost accounting. A stronger recovery — which Knight Frank's +18% to 2030 forecast implies — improves these numbers considerably. For investors who want to stress-test their own thesis before committing, our three-minute due diligence framework walks through the four quick checks every London property should pass.

Both Developments at a Glance

This is not an aggressive scenario. It uses conservative forecasts and full cost accounting. A stronger recovery — which Knight Frank's +18% to 2030 forecast implies — improves these numbers considerably. For investors who want to stress-test their own thesis before committing, our three-minute due diligence framework walks through the four quick checks every London property should pass.

The Window Closes at Completion

Off-plan pricing exists for one reason: the developer needs committed buyers before the building is finished. Once construction completes, that advantage disappears. The unit is priced at market. The flexible payment structure is gone. The choice of floor, view and aspect is whatever's left.

At Westminster Tower, several units are already sold. At Wimbledon Bridge House, two second-floor two-bedroom apartments and multiple one-bedroom units are reserved or taken.

The best way to think about this moment is simply: you are being offered the chance to buy London in 2026 for delivery in 2027–28 at prices that reflect today's softened market, not tomorrow's recovery.

Savills says 13.6% cumulative growth to 2030. Knight Frank says 18%. The Bank of England has been cutting rates since late 2025. Wage growth is forecast to outpace house prices through 2029. The structural housing deficit in London is not changing.

The only variable is whether you act now or wait for the confirmation that everyone else has already bought in.

Ready to Take the Next Step?

At Imperia Broker, we work with a limited number of clients on each development we represent. When you work with us, you receive:

- Direct developer access and early-stage pricing on launches before public release

- Full investment modelling tailored to your tax residency, currency and objectives

- Legal and compliance support from reservation through to completion, including international buyer guidance

- Full letting and property management via Staymo — short-let, mid-term and long-term strategies handled end-to-end

- Ongoing market intelligence so you know when to hold, when to sell and what to look at next

The conversation looks different depending on who you are:

- Private investors and HNWI — building or rebalancing a London portfolio

- Family offices — placing institutional capital with full IB Score underwriting

- Brokers and IFAs — partnering on London opportunities for international client books

All price forecasts cited are sourced from Savills, Knight Frank, Hamptons and Nationwide and represent market projections only, not guarantees of future performance. All rental estimates are developer-provided indicatives. Tax and legal implications vary by individual circumstances and jurisdiction. Imperia Broker recommends that all buyers take independent legal, tax and financial advice before committing to any property purchase. All property details are correct at time of publication (May 2026) and subject to change.

Sources: Savills Residential Forecasts 2026; Knight Frank UK Residential 2026; ONS UK House Price Index February 2026; London Square Westminster Tower Price List (March 2026); London Square Wimbledon Bridge House Price List (March 2026); Cushman & Wakefield Residential Forecast 2026; Intracapital Estates London Rental Yields 2025; Savills Prime Rental Market Q3 2025; Land Registry Data 2025.