Why the IB Score exists

When you book an Airbnb, you see a structured rating before you commit: stars, host rating, response rate, cleanliness, location. The system works because it's comparable — you can put three listings on the same scale at a glance, without reading every review or opening ten browser tabs.

When an investor commits two million pounds to a property, that scale doesn't exist. There's a brochure, a yield projection prepared by the seller, an opinion from a broker, sometimes a side-by-side with two or three neighbouring assets. But no single frame of reference on the buy-side that lets you see, at a glance, how this proposition compares with everything else available in London property investment today.

The IB Score is our answer to that gap. With one essential difference from Airbnb: there, the rating is given by a guest after the visit. Here, the score is built before purchase, based on the structural indicators that define investment quality — income, capital growth, liquidity, location, build, and legal safety.

Table of Contents

What the score is, and what sits beneath it

Real estate is messy. The IB Score doesn't pretend otherwise — it imposes a structure on the mess so that decisions become comparable, while the underlying complexity remains visible in the extended report.

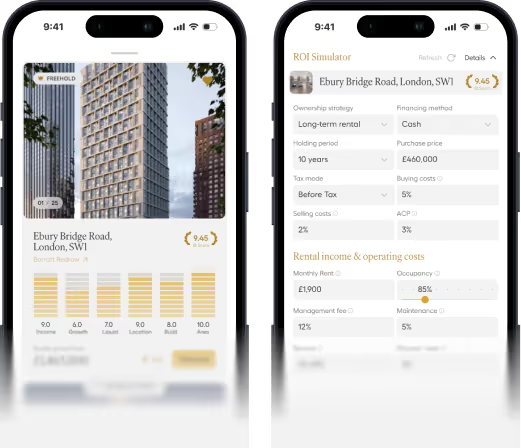

The IB Score is a single number from 1 to 10. Behind it sit six categories — what appears on the property page — and behind each category sit two sub-scores. Twelve measurable components in total. The headline score and the six category scores are public; the twelve-component breakdown, with source attribution and category-level confidence, is delivered in the extended report we prepare on request.

The weighting that turns these inputs into one score is proprietary.

How we handle uncertainty

A score is only as honest as its treatment of missing or weak data. A few principles run through the methodology.

Conservative baselines as the default. Where data is thin or missing, the calculation falls back to baselines drawn from the relevant market archetype — urban core, prime central, suburban — rather than to the developer's own projection.

Self-reported numbers stay outside the score until verified. A developer's stated yield, occupancy, or capital appreciation forecast is treated as raw input. It moves the score only when confirmed by an independent source: regulated research, transaction data, or an executed operator agreement.

Each category carries an internal confidence level. Strong data — regulated research, multiple comparables, executed agreements — supports a high-confidence score. Thin data — one comparable, a single forecast, undocumented developer claims — supports a lower-confidence score. The public score blends categories into a single number; the extended report surfaces where the data is solid and where it is thinner, so you know where to dig further.

Specific signals downgrade the score. Off-plan without escrow protection. A leasehold under 80 years. A developer with delivery delays in the track record. A single comparable instead of a pool. Each of these signals reflects a risk that historically translates into real lost returns.

The six categories

Income — what the asset actually delivers

A "yield 8%" headline rarely specifies whether the figure is gross or net, whether it includes service charges and operator commission, whether occupancy assumptions are realistic.

Cashflow Performance scores yield (gross, net, occupancy) against locally verified comparables. In London, this is anchored to Staymo's real operating data — occupancy, nightly rates, costs and void periods — across 2,000+ managed homes, so the income side reflects what comparable assets actually achieve rather than a developer's model. Total Return captures IRR, ROI, capital growth, and finance structure across the hold period. The result reflects what the owner sees on the bank statement.

What this means in practice: an asset advertised at 8% yield can land in this category materially lower once put through the methodology. The score reflects what the asset actually delivers. For a quick way to flag this gap before involving the full scoring engine, our three-minute due diligence framework walks through the basic checks any buyer should run first.

Growth — what happens over five and ten years

"+30% by completion" is a hypothesis that the category tests against regulated sources. The calculation draws on forecasts from analytical houses — Savills, Knight Frank, JLL, Colliers — combined with local price-to-income and price-to-rent ratios, supply pipeline pressure, and the market cycle phase.

Infrastructure projects count only when confirmed-funded-started. Elizabeth Line — yes. HS2 at Old Oak Common, where construction is active — yes. A tram link discussed in local press — zero weight. The areas where confirmed infrastructure is creating the largest IB Score uplifts in 2026 — Bayswater, Farringdon, Old Oak Common, Canada Water — are covered in detail in our market analysis of where London capital is flowing.

Liquidity — how quickly you can exit

The category investors most often underestimate, until exit becomes relevant.

Market Liquidity scores days-on-market for comparable assets, absorption rate, mortgage availability, and leasehold constraints. Friction Factor measures total round-trip transaction cost — purchase and sale taxes, agency fees, legal costs — as a percentage of asset value.

To make this concrete, consider two assets advertised at similar yields:

- Property A: 999-year leasehold in established central London, mortgageable to most lenders, deep buyer pool in the same building.

- Property B: shorter leasehold (under 100 years), mortgageable but with lender restrictions, thin recent comparable activity in the building.

Today the headline yield looks identical. At exit, Property A typically re-markets and sells within weeks; Property B can take months and often requires a price concession to clear. Round-trip transaction costs compound the gap further. The Liquidity score makes this gap visible before purchase.

Location — the structural factor

The only category that cannot be remediated after purchase, which is why the methodology is conservative here.

Current Location Quality scores transport access, schools (via official Ofsted ratings), local crime context (drawn from Police.uk), surrounding amenity, and infrastructure within reach. Future Mobility counts only confirmed and funded infrastructure projects, with anti-double-count logic shared between Location and Growth.

A note on crime data: in Location we treat the local crime rate as a location externality — it affects desirability and tenant demand. This is distinct from the Safety category, which scores legal and jurisdictional risk (leasehold security, rental legality, foreign ownership rules). We track both separately and avoid double-counting between them.

In London's sub-markets, this is why Westminster prime real estate and Wimbledon investment property are scored on different baselines for transport, schools, and amenity. Each area receives its own assessment across these dimensions, separate from the general 'prime London' label. For two current case studies that illustrate this — Westminster Tower (SE1) and Wimbledon Bridge House (SW19) — see our analysis of why London off-plan property is the smartest move right now.

Build — who built it and what you actually get

For off-plan and new-build assets, the Build category weighs the developer's track record from regulated sources: completed projects, delivery timelines, finish quality versus what was promised. Off-plan with escrow plus completion bond scores higher; off-plan without protection of buyer funds scores lower. London off-plan investment frequently carries 12–24 month delivery delays — a scenario rarely discussed at the point of sale, yet one that shifts the actual IRR, pushes back the exit, and extends the period when capital is frozen without rental income.

For existing stock (secondary market), the focus shifts to specification, materials, layout efficiency, natural light, ceiling height, and uniqueness within the segment. The track record question becomes "what is the condition and provenance of the building today," instead of "will the developer deliver on time."

A clarification on what "partially remediated" means in this category. It refers to cosmetic and operational layers — finish quality, layout adaptations, soft refurbishment, operator change. Structural risks operate on a different timescale. Cladding compliance (post-Grenfell EWS1 status), latent construction defects, service charge inflation driven by unfunded maintenance obligations, and obsolescence in major systems can carry costs of an entirely different magnitude. When these appear in due diligence, the Build score flags them separately rather than blending them into general "build quality."

Safety — the most structural category

In the United Kingdom, Safety rarely raises questions. The Land Registry, the English legal system, and tax transparency together establish a high baseline. This is one reason UK property investment remains a structural preference for international capital, even when other jurisdictions advertise higher yields.

When we score assets in other jurisdictions — Indonesia, Northern Cyprus, Georgia, Spain — the category effectively carries more weight in the calculation. In each of these jurisdictions, specific risks become relevant that in the UK are either absent or at a minimal level: leasehold renewal uncertainty, foreign ownership restrictions, title registration specifics, regional short-let regulations, capital controls on income repatriation.

Local Risk / Rental Legality scores the legality of short-let and long-let arrangements in the specific jurisdiction. Country Risk / Title Security analyses the title system, property rights protection, the availability of foreign ownership, and escrow provisions for off-plan. The underlying reference is World Bank Worldwide Governance Indicators on rule of law, property rights, and contract enforceability.

One clarification: we don't provide legal advice. What the Safety score flags is the level of risk and the kind of evidence required to mitigate it. For specific structuring, lease drafting, or cross-border tax questions, our role is to direct you to qualified legal counsel.

Where the IB Score works best

The United Kingdom is our core market. The Land Registry has provided public transaction data since 1995. The ONS publishes a rental price index by postcode district. Ofsted issues official school ratings. Police.uk publishes crime statistics. The EPC register exposes the energy efficiency of every individual property.

This density of regulated data lets the methodology operate at high confidence across all six categories — a structural advantage that international investors often underestimate when comparing yields on a spreadsheet alone. Our catalogue centres on residential investment property in London and across the UK. We are willing to score assets outside the UK on request; the methodology produces its sharpest signal where the data is deepest.

What the investor gets

A common language. Three assets in three countries, under three tax regimes and three forms of ownership, can be compared in a single frame of reference — by yield, liquidity, and risk.

A defensible decision. A figure backed by six categories and twelve sub-scores with named sources withstands a conversation with a partner, a lawyer, or a financial advisor. A "+30%" marketing claim rarely passes the same scrutiny.

An improvement map. The methodology shows not only the current state of an asset but the steps that can lift the score: a signed operator agreement instead of an LOI, a verified rental track record, escrow protection on off-plan, a longer leasehold. The transaction becomes a process with clear improvement points.

Early risk indicators. An asset scoring 5.3 calls for a different level of due diligence than one scoring 7.85. The methodology surfaces the gap before capital is committed.

Where the limits are

The IB Score structures what is known about the asset today. The future remains an area with its own uncertainty — macroeconomic shifts, policy changes, and market cycles can change the picture independently of input model quality.

The IB Score is profile-agnostic. It scores the asset's structural quality, not its fit to a specific investor mandate. A capital preservation buyer, a yield-focused investor, and an opportunistic allocator may weight the same score differently. The extended report breaks the score into its twelve components precisely so an investor can re-weight against their own strategy.

The IB Score is a structured analytical framework — not yet a back-tested predictive model. We track scoring against realised performance across our catalogue, and the methodology will refine as the evidence base grows. Anyone using the score should treat it as decision support, not as a substitute for personal underwriting or independent advice.

The figure always sits alongside the investor's own context. An asset scoring 6.4 that aligns precisely with a buyer's lifestyle, time horizon, and geographic priorities can be the better choice than a 7.85 asset that is technically stronger but doesn't fit the profile. The methodology gives you the figure. The decision stays with the investor.

Further reading

For readers who want to look under the bonnet:

- IB Score Methodology Reference — full scoring mechanics, source governance, confidence framework, market archetype baselines, and edge case handling.

- Sample Extended Report — an anonymised analysis of a real underwriting case, showing how the twelve sub-scores combine in practice.

- Glossary of Terms — reference for the technical vocabulary used across our analysis.

Want to see the IB Score on a specific asset?

Every investment property in our catalogue runs through the IB Score before publication. If you have a proposal from elsewhere — a developer brochure, an off-market introduction, a private broker's pitch — we can calculate the IB Score, walk through the twelve sub-scores, and identify both the strengths and the risk zones.

Yield and capital growth forecasts referenced in the methodology are indicative. Past performance is not a guarantee of future returns. For legal and tax questions we direct you to qualified counsel.

Who we work with:

- Private investors — bespoke London portfolios

- Family offices — institutional mandates with full IB Score analysis

- Brokers — partnering on London opportunities for international client books