Ask most people whether now is the moment to buy in London and the instinct is to wait. The headlines point one way: soft prices, thin transaction volumes, a decade in which the rest of the UK pulled ahead. The data on the London property market points somewhere more useful. The Bank of England base rate has eased to 3.75%, held in June 2026, after the sharpest tightening cycle in a generation. Prime central London values sit roughly 24.5% below their 2014 peak (Savills, 2026). And the capital's structural shortage of new homes has not moved. For the international investor, the distance between how this market feels and what the numbers show is where the opportunity sits.

This article is not a price forecast. The London property market forecast 2026 to 2030 sets out the five-year, segment-by-segment trajectory. This piece answers a narrower and more practical question: is now a good time to buy property in London, and on what terms? The short answer is yes, for a long-horizon investor buying the right asset. The rest of this article explains why, where the case is weaker, and what would prove it wrong.

Table of Contents

The Short Answer: Is Now a Good Time to Buy in London?

Yes, for investors with a five-year-plus horizon buying high-quality assets. Three structural forces support acting now rather than waiting for a clearer signal that may never arrive:

- Rates have turned. The Bank of England base rate has stabilised at 3.75% (held June 2026), down from the 2023 to 2024 peaks, which lets an investor underwrite a purchase with confidence.

- Supply stays tight. London's assessed housing need runs at roughly 88,000 homes a year, and delivery has fallen well below that level for a decade, supporting values over the medium term.

- Demand is returning. International buyers, particularly from the UAE and Hong Kong, are re-entering selectively from a low base, helped by sterling positioning and London's long-term safe-haven status.

The answer becomes "wait" in two cases: a weak asset, or a horizon shorter than three to five years. In a market still finding its floor, near-term softness can outweigh the structural supports, and thin liquidity penalises anyone who needs a fast sale. Choosing the asset matters more than timing the entry.

What the Data Says Right Now

The case rests on three readings. A disciplined argument states each one plainly rather than selecting only the flattering figures.

Read together, these point to a market that has repriced rather than one that is failing. Financing has settled, prices sit below where they were a decade ago, and the supply shortfall keeps a floor under well-specified homes. For the full five-year price outlook, see the London property market forecast 2026 to 2030 rather than repeating its tables here.

Are London house prices falling? Modestly, and unevenly. Some indices record annual softness of 2 to 3%, concentrated in flats rather than houses. This reflects adjustment to higher rates and greater stock availability, not structural weakness. For a buyer with time on their side, this softness reads as negotiating room, not a reason to stay out.

Should I Invest in London Property, or Wait?

The decision turns on horizon and asset quality, not on a single verdict about London as a whole. Framed correctly, the question is not "London or not" but "which London asset, and on what terms".

The case for acting now rests on four supports:

- Rate stability removes much of the uncertainty that kept buyers on the sidelines through 2023 and 2024.

- Chronic undersupply keeps pressure under values across the hold period.

- Currency positioning gives buyers in AED, HKD, or USD an improved entry point against sterling.

- Off-plan and new-build stock, already compliant with tightening energy standards, sits where the professional end of the market is concentrating.

The risks deserve equal weight:

- The additional-property stamp duty surcharge adds 5% to every band for investors buying beyond a primary home, with a further 2% for non-UK residents. On a £600,000 flat, the additional-property surcharge alone adds £30,000 to the entry cost, so the asset has to work harder to justify the outlay.

- A shorter holding period exposes the buyer to further near-term softness and to the high transaction costs that make London a poor market for quick resale.

These are not reasons to avoid London. They are reasons to be precise about the asset and the timeframe. Two flats a few miles apart can behave like different asset classes: one a resilient income asset, the other an illiquid holding that erodes through a soft cycle. Before committing capital, an investor can compare live London stock on Imperia Broker's investment platform and test each opportunity against the same structural criteria.

What Would Prove This Thesis Wrong?

A useful thesis states the conditions under which it fails. Three developments would shift the answer from "buy now" back to "wait", and an investor holding London stock should track each one:

- Rates reverse upward. If the Bank of England is forced to raise the base rate materially above 3.75% to counter renewed inflation, borrowing costs climb again and the affordability case behind current pricing weakens.

- Supply catches up with need. If new-build delivery moves back toward the roughly 88,000 homes a year London requires, the structural scarcity that supports values over the hold period would ease, and with it the floor under quality stock.

- Demand stalls rather than returns. If international buyers stay on the sidelines and domestic demand softens together, the thin liquidity that already penalises quick sales deepens, and near-term price softness could run longer than a five-year horizon absorbs.

None of these is the base case as of mid-2026. Rates have stabilised, delivery remains well short of need, and overseas demand is returning from a low base. But an investor who cannot answer what would change their mind is not holding a thesis, only a preference. If two or more of these conditions turn together, the disciplined response is to wait.

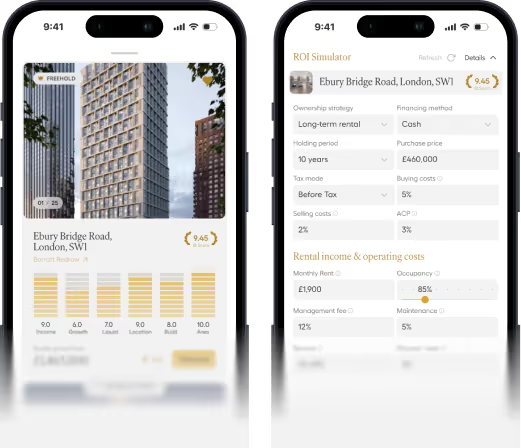

Where IB Score Fits the Timing Question

A market-level signal, whether a discount, a rate cut, or a supply gap, tells an investor nothing about whether a specific flat is the right buy. Closing that gap is the purpose of the IB Score, Imperia Broker's investment rating built on operational data from the 2,000+ London properties managed by Staymo, the London short-let operator that backs Imperia Broker, together with regulated UK datasets. It rates a specific asset across six structural factors:

- Income: how much the property generates and how stable that income is

- Growth: the potential for the property's value to increase

- Liquidity: how easily and quickly the property can be sold

- Location: quality of the location today and looking ahead

- Build: build quality and developer track record

- Safety: title security, legality of rental, and country risk

For the timing question, the value is specific. In a softer market, a high Income and Liquidity profile is what buffers an asset against near-term price movement. Managed rental performance holds even when sales values drift, and a deep buyer pool preserves the exit. An asset that scores well on those factors supports a "buy now" decision for a long-horizon investor in a way that a low-scoring holding in a thin micro-market does not, however attractive the headline price looks. The full methodology is set out in Inside the IB Score, and you can see how it applies to live stock across our London investment opportunities.

A worked example makes the point. Take a one-bedroom flat at Wimbledon Bridge House, which carries an IB Score of 8.0 with Liquidity leading at 9.0. That profile describes an asset with a deep, active buyer pool and stable managed rental income, exactly the combination that holds up when sales values drift. For a long-horizon investor, this is a "buy now" asset: near-term softness is cushioned by income, and the exit stays open if plans change.

Contrast that with a superficially similar flat in a thin micro-market, where a low headline price masks a Liquidity score closer to 4.0 and shallow rental demand. The same 2 to 3% market softness that reads as a negotiating opportunity on the first asset becomes a trap on the second, because there is no ready buyer at the point of exit. Two flats, a comparable asking price, opposite timing answers. That is what "asset selection matters more than timing" means in practice.

FAQ

Is now a good time to buy property in London?

Yes, for long-horizon investors buying high-quality assets. With the Bank of England base rate eased to 3.75% (held June 2026) and London new-build supply running well below the roughly 88,000 homes a year the capital needs, current conditions create a favourable entry window for buyers holding five years or more. The case is weaker for short-horizon buyers or for weak assets, where near-term softness and high transaction costs carry more weight.

Is now a good time to buy a house in the UK?

Broadly yes, with rates stabilising at 3.75% and affordability improving gradually, though outcomes vary by location. London stands apart for the international investor: its structural supply shortage and long-term capital-growth potential distinguish it from regional markets, even while near-term prices stay soft. As across the UK, the outcome depends far more on asset selection than on market timing.

Should I invest in London property in 2026?

For investors who select assets rigorously, yes. London typically delivers lower rental yields than many regional cities, often in the region of 3 to 4%, but compensates through stronger long-term capital growth, deeper liquidity, and sustained international demand. The IB Score framework weighs those trade-offs on consistent criteria rather than headline pricing.

Are London house prices falling?

Modestly. Recent indices show annual softness of 2 to 3% in some periods, concentrated in flats rather than houses, and reflecting adjustment to higher rates rather than a broad decline. For a buyer with a five-year-plus horizon, this softness reads as an entry point, supported by a structural supply shortage expected to underpin values over time (ONS, 2026).

Conclusion

2026 is a pragmatic entry window for the disciplined, long-horizon investor in London property. Stabilising rates, a measurable pricing discount, and an unresolved supply shortage reward selective buying over blanket caution, provided the asset is right and the horizon is long. Broad market appreciation is not this cycle's story. Asset selection is. The investor who can name the asset they are buying, the reasons behind it, and the conditions that would change their mind is making a decision. Everyone else is only guessing at the bottom of the market.