Central London flats have an image problem. After a decade in which the rest of the UK pulled ahead, the segment is widely written off as overpriced, illiquid and going nowhere. The data on the central London property market tells a more nuanced story. Prime central London values ended 2025 around 24.5% below their 2014 peak (Savills, 2026) — a measurable discount, not a vague claim — while buyer activity has begun to turn up from a low base and the capital's long-run shortage of new homes persists. That gap between what the market feels like and what the numbers show is the whole argument of this piece.

Turning a market-wide discount into a decision still requires a tool. That tool is the IB Score — Imperia Broker's 1-to-10 investment rating, built on open-market and regulated UK data (Land Registry, ONS, Ofsted, Police.uk) together with Staymo's real operating data across its 2,000+ managed London properties. It rates a specific flat across six structural factors — Income, Growth, Liquidity, Location, Build and Safety — so a market-level signal becomes a property-level judgement.

Table of Contents

How IB Score Reads the Central London Property Market

Before any number, one discipline: "good" is not a property of the asset. It depends on what the investor is optimising for. A buyer chasing monthly income, a buyer chasing capital growth, and a buyer who needs to exit quickly are looking at the same flat through three different lenses — and the same central London property can be a strong buy for one and a poor fit for another.

The IB Score makes those lenses explicit. Every asset is scored on the same six factors, applied consistently, so two flats in two postcodes can be compared in a single frame:

The point of the framework is comparability. The rest of this article looks at where central London flat prices actually sit, what is happening to demand and supply, and where the forecasts point — and then applies the six factors to a real asset.

Central London Flat Prices: Where They Stand

The headline discount is real. Prime central London values fell 4.8% in 2025 and finished the year roughly 24.5% below their 2014 peak, according to Savills (2026); Knight Frank puts the fall from 2014 at around 22%. Coutts, using its own client index, had prime London 13.2% below its Q2 2014 peak in its Q1 2026 reading (down from a 10.3% gap in late 2025, as further Q1 falls widened the discount) — leaving prices around 2013 levels. The exact figure varies by basket: the wider the index reaches into more resilient outer-prime areas, the smaller the gap looks. But every credible index agrees on the direction: this is a segment priced well below where it was a decade ago.

Within that, flats have lagged houses — and that lag is most of why central London property looks weak on the surface. UK House Price Index data shows London flats falling around 5% over the past year while terraced houses edged higher, and ONS recorded flats and maisonettes as the weakest property type nationally, down 3.8% in the year to February 2026. Savills attributes the underperformance to thinner buy-to-let demand; rising service charges and leasehold uncertainty add to it. In short, the part of the market dragging london flat prices down is precisely the part this article is about.

Step back to the wider capital and the same weakness shows up in the aggregates. London house prices have been broadly flat to slightly lower over the past year, and London property prices across all types fell around 2–3% in the year to early 2026 (ONS, 2026) — leaving the London housing market among the softest of any UK region. For a buyer scanning listings, the typical flat for sale in London now sits near £420,000–£450,000 (HM Land Registry, 2026), but that average hides a wide gap between a discounted central flat and an outer-borough house.

Demand and Supply: What Is Actually Happening

Three signals matter here, and a balanced reading of each is what makes the discount argument credible rather than promotional.

Supply: a sharp contraction, then a rebound

The supply story turned twice in six months, and getting it right matters. Ahead of the 2025 Autumn Statement, prime London listings contracted sharply — Coutts reported new listings down 35% quarter-on-quarter in late 2025, one of the steepest year-end slowdowns since the pandemic. Then deferred sellers returned: in Q1 2026, Coutts recorded new instructions up 49% quarter-on-quarter, with available stock around 6% higher than a year earlier. So buyers still have choice today — the cyclical squeeze eased. What has not changed is the structural picture: London consistently builds far fewer homes than it needs (the Greater London Authority targets 52,000 a year against completions nearer 35,000), which keeps a long-run floor under quality stock even when short-term supply swings.

Buyer interest is turning — early, and from a low base

This is where overstatement would be easy and wrong. Completed transactions are still weak: LonRes recorded prime London sales down 32.6% year-on-year in Q1 2026, the lowest quarterly volume since the pandemic. But the leading indicators have moved. Coutts logged 841 prime transactions under offer by the end of Q1 — its highest Q1 figure in over a decade — and LonRes put Q1 under-offers up 7.6% year-on-year and around 35% above the pre-pandemic average. Conveyancing and survey registrations jumped sharply at the start of the year (Reallymoving), and prime agents report client enquiries up by double digits. The measured reading: confidence is returning ahead of completed volume, and the recovery is real but early-stage.

International demand remains a structural force

Central London's flat market is not a domestic story alone. International buyers account for more than half of sales in the most affluent central postcodes, with US and Middle Eastern buyers dominating the super-prime end, and a weaker pound improving entry economics for dollar-denominated purchasers. The picture is genuinely two-sided: the phasing-out of non-dom status and the 2% overseas Stamp Duty surcharge have cooled some international activity, and roughly 60% of current prime buyers are UK-based owner-occupiers (Winkworth). For overseas holders, the 999-year leases attached to new prime stock — long-valued by Hong Kong buyers in particular — remove the leasehold-runway risk that weighs on older flats. The drivers behind landlord selling and the broader shift in investor behaviour are covered in our analysis of why landlords are selling up.

The Outlook: What the Forecasts Say

The major houses agree on the shape, and it is sober rather than rosy. For prime central London specifically, Savills forecasts a further −2% in 2026, flat in 2027, then a gradual recovery totalling roughly +8.1% over the five years to 2030. Knight Frank's spring 2026 revision similarly pencils in −2% for prime central London in 2026, with the bulk of its growth weighted to 2029–2030 (around +4.5% and +6%). Neither sees a bounce; both see a floor in 2026 and an upward trajectory thereafter.

For an investor, the takeaway is specific: a lagging segment, with a measurable discount and early signs of demand returning, is an entry-window argument for a long-term hold — not a quick flip. The capital appreciation case is structural and back-loaded, which is exactly why holding period and asset selection matter more than market timing. For the full five-year, segment-by-segment picture, see our London property market forecast 2026–2030.

What could invalidate this thesis? A disciplined case should be explicit about what would prove it wrong. Persistently high interest rates, a deeper contraction in international demand, or further tax changes affecting high-value residential property could each delay the expected recovery. None of these would overturn the long-term case on its own — but together they are the reason individual asset selection matters more than broad market timing.

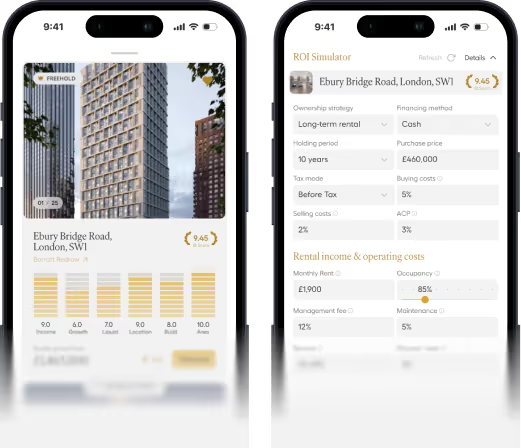

IB Score in Action: Westminster Tower

A market-level discount tells you nothing about whether a specific flat is the right buy. That is the question the IB Score answers. Take Westminster Tower — a prime riverside new-build on the Albert Embankment (SE1), developed by London Square (part of the Aldar Group), with a 999-year lease and Thames-facing views toward the Palace of Westminster.

Taken factor by factor, the scorecard does not flatter — it explains. Location, build and safety score high because the address, the developer and UK title law genuinely are strong. Growth sits at a moderate 6.0 because much of the investment case rests on preserving purchasing power and participating in a gradual recovery, rather than capturing rapid price appreciation. Income and liquidity are lower for structural reasons, not weakness: Westminster Tower's gross yield sits in the high-2% to low-3% range — typical for a prime new-build trophy asset, and below the roughly 3–5% the wider prime London market spans depending on location, asset type and management — while liquidity is constrained less by demand than by high transaction costs and premium pricing. These are the trade-offs of a capital-preservation asset, and the score states them plainly. The full mechanics — twelve sub-scores, source governance, confidence levels — are set out in our IB Score methodology.

FAQ

Is London property a good investment in 2026?

London property remains a long-term capital-growth and capital-preservation play rather than a high-yield one — gross yields at the prime end typically run in the 3–5% range, below what regional UK or outer London can offer. What 2026 adds is a measurable entry discount, concentrated in central London flats: prime central values sit roughly 24.5% below their 2014 peak (Savills), buyer demand is turning from a low base, and forecasters see a floor this year with growth weighted to later years. Whether a particular flat is a good buy is a question the IB Score is designed to answer across six factors. You can request one at imperiabroker.com/invest.

Are London house prices falling?

London house prices have been broadly flat to slightly lower over the past year — but the real weakness is in flats, not houses. UK House Price Index data shows London flats down around 5% over the past year while terraced houses edged higher, and inner-London flats sit about 11% below their April 2020 level (E.surv, April 2026). Outer-London flats have held up better. The decline is also showing signs of slowing as buyer activity returns, though completed-transaction volumes remain low. The flat market, in other words, is where the discount is — and where selective buyers are looking.

Is now a good time to buy property in London?

For a long-term holder, the conditions are more favourable than they have been in years: a deep discount to the 2014 peak, buyer demand turning up from a low base, and a Bank of England base rate that has eased to 3.75% (held in June 2026). The case is weaker for anyone needing a quick resale, given high transaction costs and a recovery that forecasters weight toward 2028–2030. As ever, the answer depends on the specific asset, its lease and its economics — which is what a property-level rating exists to test.

Why are central London flats cheaper than they were?

A combination of factors, most of them straightforward to name. Tax and regulatory change over the past decade — higher stamp duty on additional and high-value homes, the phasing-out of non-dom status, and tighter buy-to-let economics — pulled back the international and investor demand that once drove the segment. A post-pandemic preference for space shifted buyers toward houses. Rising service charges and leasehold uncertainty weighed on flats specifically. The result is a segment that has lagged both the wider UK and London's own housing market for years, leaving today's prices well below their previous peak.

How do I tell if a central London flat is a good buy?

The answer is in the data, not the brochure. A reliable assessment runs the asset across the same structural factors every time: Income, Growth, Liquidity, Location, Build and Safety. That means checking whether the quoted yield is gross or net of service charges and management, how the lease and transaction costs affect exit, what confirmed infrastructure actually supports the location, and how secure the title is. Our three-minute due-diligence framework covers the first quick checks; the IB Score turns them into a single comparable rating.

The perception of central London flats lags the data. With central London flats for sale at a measurable discount to their 2014 peak, buyer interest returning early, and a structural shortage of new homes behind them, the segment rewards selective buying over blanket caution. The disciplined way to invest in London property in this market is to let a consistent rating — not a brochure — make the selection objective.

See how the rating works on any asset: Inside the IB Score.

All forecasts cited are market projections from Savills, Knight Frank and Coutts and are not guarantees of future performance. Price and discount figures are drawn from the sources named in-text and were current as of June 2026. Imperia Broker recommends independent legal, tax and financial advice before any purchase.