London remains structurally undersupplied at a housing level, particularly in Zones 1–3 where demand continues to outpace new completions. Recent data from the Office for National Statistics shows London house prices remain significantly higher than the UK average, with annual growth returning unevenly across boroughs depending on regeneration, transport connectivity and supply pipelines (UK House Price Index, March 2026).

For international investors comparing the best areas to invest in London property, headline averages are no longer sufficient. Two postcodes can sit only a few miles apart yet behave like entirely different asset classes. That is why area selection for London property investment 2026 needs to be analytical rather than descriptive.

This article uses the IB Score framework to evaluate London property investment areas consistently across six factors: income, growth, liquidity, location, build quality and safety.

Table of Contents

What Makes an Area a Good Investment?

The concept of the "best areas to invest in London property" depends entirely on investor objectives. A high-yield location may not deliver capital growth, while a prime zone may offer liquidity and long-term stability but lower income returns. As a result, comparing London property investment areas requires a consistent scoring model rather than subjective ranking.

The IB Score framework addresses this by assessing each area across six factors:

In 2026, this framework is particularly relevant due to two structural forces. First, interest rate stabilisation following the Bank of England's tightening cycle has improved investor confidence but has not fully restored affordability (Bank of England, 2026). Second, a supply gap across Zones 1–3 continues to support pricing floors, while off-plan discounts remain available ahead of 2027–2028 completions.

The result is a market where timing and location selection matter more than ever, and where "best places to invest in London property" cannot be defined without a structured analytical lens.

Best Areas to Invest in London Property: IB Score Breakdown

To identify the best London boroughs to invest in property and the best places to invest in London property, investors need to look beyond headline pricing and assess factors such as income potential, growth prospects, liquidity and location quality. The following areas are evaluated using the IB Score framework.

Wimbledon (SW19)

Wimbledon represents a premium outer-zone market with strong capital preservation characteristics and is often considered a key location for Wimbledon investment property. It also appeals to international buyers, particularly Hong Kong investors, due to its 999-year lease structures and long-term ownership security. Selective premium off-plan developments also sit within the market, offering stability with limited exposure to short-term volatility rather than high-growth upside.

Average property values sit at £860,949, with a gross yield of 2.9%. Demand is supported by rail connectivity into central London in under 20 minutes and consistent family-driven buyer interest. The area shows stable pricing with limited volatility compared to central zones. Within the IB Score framework, Wimbledon scores strongly on location and build quality due to established infrastructure and reputable development standards.

Westminster (SW1)

Westminster remains one of the most internationally recognised ultra-prime markets in London. Average property values sit at £998,154, with a gross yield of 3.8%.

While the latest data shows a Year-on-Year (YoY) decline of 19%, this represents a prime market characterised by high entry pricing, institutional demand and strong global liquidity. Recent price adjustments reflect a sharper correction cycle than other London segments, driven by a post-pandemic recalibration of ultra-prime valuations and shifting international capital flows.

For the strategic investor, this sharp correction cycle should be viewed as a significant entry opportunity rather than a long-term risk. Because Westminster retains long-term appeal and a dedicated international buyer base, buying into this dip allows investors to acquire premium capital assets at a cyclical discount before the market stabilises.

Within IB Score terms, Westminster remains heavily driven by location, safety and liquidity strength.

East London (Zone 2–3)

East London continues to rank among the most active London property investment areas, particularly for investors focused on yield-led strategies and long-term income growth. It remains a core location for East London property investment, driven by strong rental demand and ongoing regeneration.

Average property values sit at £531,993, with a gross yield of 5.4%.

Stratford continues to benefit from sustained regeneration following the Queen Elizabeth Olympic Park legacy and ongoing commercial expansion.

The Elizabeth Line has also improved connectivity, with Transport for London reporting significant journey time reductions across East London corridors (TfL, 2025). This has supported tenant demand and strengthened rental performance.

Within IB Score terms, East London is weighted towards income and growth, reflecting its regeneration-led trajectory and leading yield profile.

South East London (Greenwich, Lewisham)

South East London is increasingly relevant in searches for up and coming areas London, driven by relative affordability compared to Zones 1–2 and a strong development pipeline.

Average property values sit at £576,583, with a gross yield of 3.8%.

Greenwich continues to benefit from long-term regeneration and riverside development, while Lewisham has seen increased planning approvals for mixed-use residential schemes (GLA).

Within the IB Score framework, this region reflects a growth-led profile supported by infrastructure expansion and relative affordability.

North London (Islington, Hackney)

North London remains one of the most resilient segments of the London market for rental demand.

Average property values sit at £800,865, with a gross yield of 2.9%.

Hackney and Islington both show strong rental stability, supported by established transport links and sustained professional tenant demand. However, yields are lower than in regeneration-led zones, reflecting its stability-led rather than yield-led profile.

Within IB Score terms, North London performs strongly on income stability and liquidity rather than yield maximisation.

Table 1: Best London Boroughs to Invest in Property

Up and Coming London Areas: What the Data Shows

Up and Coming London Neighbourhoods: The Infrastructure Effect

The Elizabeth Line has been one of the most significant drivers of up and coming areas in London, with major journey time reductions and increased passenger flows across Zone 2–3 stations (TfL, 2025). Areas along the line have recorded above-average price growth compared to wider London averages.

Regeneration Pipeline

London continues to deliver large-scale residential regeneration schemes across East and South East boroughs, particularly in Stratford, Lewisham and Woolwich (GLA, 2025). These pipelines increase future housing supply while also driving near-term investment activity.

Rental Demand Shift

Affordability constraints in central London have driven tenant migration towards Zones 2–3. This has increased rental demand in East and South East London, supporting yield compression in established regeneration zones and reinforcing their role as entry points for investors.

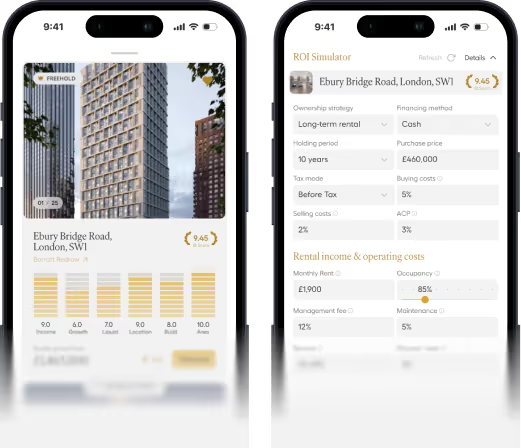

IB Score in Action: Westminster Tower

Investors often struggle with comparing assets such as Wimbledon and East London because price per square foot does not capture income stability, liquidity or risk profile. The IB Score methodology solves this by applying a consistent evaluation framework.

Below is the Westminster Tower scorecard:

The scorecard highlights a clear profile: strong location, build quality and safety underpin long-term stability, while income and liquidity reflect the structural characteristics of prime new-build assets rather than underperformance. This level of transparency allows investors to compare London property investment areas on a like-for-like basis.

Further detail on the methodology is available in our IB Score methodology.

FAQ

What are the best areas to invest in London property in 2026?

The answer depends on investment objective. For yield, East London and South East London typically perform better due to stronger rental demand and lower entry prices. For capital preservation, Westminster and Wimbledon remain preferred due to stability and international demand. The IB Score framework sets out these trade-offs using consistent data inputs, with a full breakdown of locations available in our London investment guide.

Is now a good time to buy property in London?

Market conditions in 2026 reflect stabilising interest rates and continued supply constraints across Zones 1–3. This supports long-term investment cases, particularly in areas with regeneration pipelines. However, short-term performance varies by borough and asset type, especially between prime and emerging markets.

Where are up and coming areas in London for property investment?

East London (Zone 2–3) and South East London regeneration corridors remain the primary up and coming areas London investors focus on. East London, including regeneration hubs like Stratford, is supported by Elizabeth Line connectivity and records a gross yield of 5.4%, reflecting strong rental demand and capital growth potential. South East London, including locations like Lewisham, continues to benefit from regeneration activity and planning growth, with a gross yield of 3.8%. These areas prioritise growth over immediate liquidity compared to more established London markets.

How do I know if a London property is a good investment?

A property should be assessed across multiple factors rather than price alone. The IB Score evaluates income, growth, liquidity, location, build quality and safety to provide a structured comparison. This reduces reliance on subjective judgement and improves consistency across London property investment areas. This framework can also help investors determine where to invest in London property based on their individual goals and risk profile.

Is London property a good investment compared to regional cities?

London typically delivers lower rental yields than many regional UK cities but compensates through stronger long-term capital growth and international demand. It also benefits from deeper liquidity and structural supply constraints, which support long-term value retention. Compared to regional markets, London also has additional structural advantages, including sustained overseas buyer interest and, in some segments, long leasehold structures such as 999-year terms that are particularly attractive to international investors, including buyers from Hong Kong.

Conclusion

Selecting the best areas to invest in London property in 2026 requires more than identifying growth hotspots. It requires structured evaluation across income, growth and risk factors, particularly in a market shaped by supply constraints and infrastructure-led change.

The IB Score provides a consistent way to assess where to invest in London property based on measurable criteria rather than narrative trends.

Disclaimer: This blog is for informational purposes only and should not be taken as financial or investment advice. Readers should seek independent professional advice where required.